About the Federal Reserve System

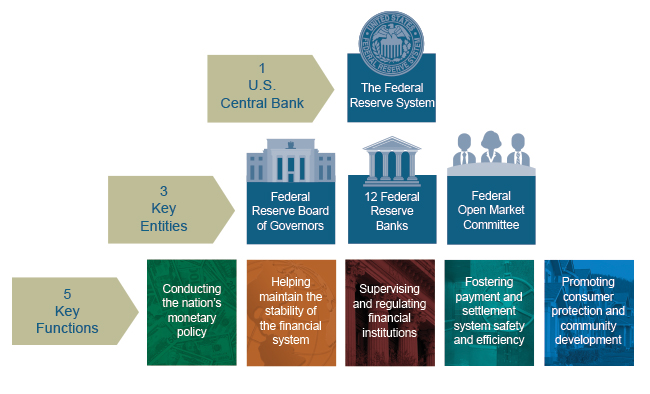

The Federal Reserve System is the central bank of the United States.

It performs five general functions to promote the effective operation of the U.S. economy and, more generally, the public interest. The Federal Reserve

- conducts the nation's monetary policy to promote maximum employment, stable prices, and moderate long-term interest rates in the U.S. economy;

- promotes the stability of the financial system and seeks to minimize and contain systemic risks through active monitoring and engagement in the U.S. and abroad;

- promotes the safety and soundness of individual financial institutions and monitors their impact on the financial system as a whole;

- fosters payment and settlement system safety and efficiency through services to the banking industry and the U.S. government that facilitate U.S.-dollar transactions and payments; and

- promotes consumer protection and community development through consumer-focused supervision and examination, research and analysis of emerging consumer issues and trends, community economic development activities, and the administration of consumer laws and regulations.

Read more in the 11th edition of Federal Reserve System The Fed Explained.

The Decentralized System Structure and Its Philosophy

In establishing the Federal Reserve System, the United States was divided geographically into 12 Districts, each with a separately incorporated Reserve Bank. District boundaries were based on prevailing trade regions that existed in 1913 and related economic considerations, so they do not necessarily coincide with state lines.

Federal Reserve Banks

The Federal Reserve officially identifies Districts by number and Reserve Bank city.

In the 12th District, the Seattle Branch serves Alaska, and the San Francisco Bank serves Hawaii. The System serves commonwealths and territories as follows: the New York Bank serves the Commonwealth of Puerto Rico and the U.S. Virgin Islands; the San Francisco Bank serves American Samoa, Guam, and the Commonwealth of the Northern Mariana Islands. The Board of Governors revised the branch boundaries of the System in February 1996.

As originally envisioned, each of the 12 Reserve Banks was intended to operate independently from the other Reserve Banks. Variation was expected in discount rates--the interest rate that commercial banks were charged for borrowing funds from a Reserve Bank. The setting of a separately determined discount rate appropriate to each District was considered the most important tool of monetary policy at that time. The concept of national economic policymaking was not well developed, and the impact of open market operations--purchases and sales of U.S. government securities--on policymaking was less significant.

As the nation's economy became more integrated and more complex, through advances in technology, communications, transportation, and financial services, the effective conduct of monetary policy began to require increased collaboration and coordination throughout the System. This was accomplished in part through revisions to the Federal Reserve Act in 1933 and 1935 that together created the modern-day Federal Open Market Committee (FOMC).

The Depository Institutions Deregulation and Monetary Control Act of 1980 (Monetary Control Act) introduced an even greater degree of coordination among Reserve Banks with respect to the pricing of financial services offered to depository institutions. There has also been a trend among Reserve Banks to centralize or consolidate many of their financial services and support functions and to standardize others. Reserve Banks have become more efficient by entering into intra-System service agreements that allocate responsibilities for services and functions that are national in scope among each of the 12 Reserve Banks.

The U.S. Approach to Central Banking

The framers of the Federal Reserve Act purposely rejected the concept of a single central bank. Instead, they provided for a central banking "system" with three salient features: (1) a central governing Board, (2) a decentralized operating structure of 12 Reserve Banks, and (3) a combination of public and private characteristics.

Although parts of the Federal Reserve System share some characteristics with private-sector entities, the Federal Reserve was established to serve the public interest.

There are three key entities in the Federal Reserve System: the Board of Governors, the Federal Reserve Banks (Reserve Banks), and the Federal Open Market Committee (FOMC). The Board of Governors, an agency of the federal government that reports to and is directly accountable to Congress, provides general guidance for the System and oversees the 12 Reserve Banks.

Within the System, certain responsibilities are shared between the Board of Governors in Washington, D.C., whose members are appointed by the President with the advice and consent of the Senate, and the Federal Reserve Banks and Branches, which constitute the System's operating presence around the country. While the Federal Reserve has frequent communication with executive branch and congressional officials, its decisions are made independently.

The Three Key Federal Reserve Entities

The Federal Reserve Board of Governors (Board of Governors), the Federal Reserve Banks (Reserve Banks), and the Federal Open Market Committee (FOMC) make decisions that help promote the health of the U.S. economy and the stability of the U.S. financial system.

Other Significant Entities Contributing to Federal Reserve Functions

Two other groups play important roles in the Federal Reserve System's core functions:

- depository institutions--banks, thrifts, and credit unions; and

- Federal Reserve System advisory committees, which make recommendations to the Board of Governors and to the Reserve Banks regarding the System's responsibilities.

Depository Institutions

Depository institutions offer transaction, or checking, accounts to the public, and may maintain accounts of their own at their local Federal Reserve Banks. Depository institutions are required to meet reserve requirements--that is, to keep a certain amount of cash on hand or in an account at a Reserve Bank based on the total balances in the checking accounts they hold.

Depository institutions that have higher balances in their Reserve Bank account than they need to meet reserve requirements may lend to other depository institutions that need those funds to satisfy their own reserve requirements. This rate influences interest rates, asset prices and wealth, exchange rates, and thereby, aggregate demand in the economy. The FOMC sets a target for the federal funds rate at its meetings and authorizes actions called open market operations to achieve that target.

Advisory Councils

Five advisory councils assist and advise the Board on matters of public policy.

- Federal Advisory Council (FAC). This council, established by the Federal Reserve Act, comprises 12 representatives of the banking industry. The FAC ordinarily meets with the Board four times a year, as required by law. Annually, each Reserve Bank chooses one person to represent its District on the FAC. FAC members customarily serve three one-year terms and elect their own officers.

- Community Depository Institutions Advisory Council (CDIAC). The CDIAC was originally established by the Board of Governors to obtain information and views from thrift institutions (savings and loan institutions and mutual savings banks) and credit unions. More recently, its membership has expanded to include community banks. Like the FAC, the CDIAC provides the Board of Governors with firsthand insight and information about the economy, lending conditions, and other issues.

- Model Validation Council. This council was established by the Board of Governors in 2012 to provide expert and independent advice on its process to rigorously assess the models used in stress tests of banking institutions. Stress tests are required under the Dodd-Frank Wall Street Reform and Consumer Protection Act. The council is intended to improve the quality of stress tests and thereby strengthen confidence in the stress-testing program.

- Community Advisory Council (CAC). This council was formed by the Federal Reserve Board in 2015 to offer diverse perspectives on the economic circumstances and financial services needs of consumers and communities, with a particular focus on the concerns of low- and moderate-income populations. The CAC complements the FAC and CDIAC, whose members represent depository institutions. The CAC meets semiannually with members of the Board of Governors. The 15 CAC members serve staggered three-year terms and are selected by the Board through a public nomination process.

- Insurance Policy Advisory Committee (IPAC). This council was established at the Board of Governors in 2018 by section 211(b) of the Economic Growth, Regulatory Relief, and Consumer Protection Act. The IPAC provides information, advice, and recommendations to the Board on international insurance capital standards and other insurance issues.

Federal Reserve Banks also have their own advisory committees. Perhaps the most important of these are committees that advise the Banks on agricultural, small business, and labor matters. The Federal Reserve Board solicits the views of each of these committees biannually.